If the administration can't make headway in curbing the cost of pensions and health care costs for retirees through negotiations, then City Council President Steve Merolla said he's ready to step in and do it by ordinance.

This item is available in full to subscribers.

We have recently launched a new and improved website. To continue reading, you will need to either log into your subscriber account, or purchase a new subscription.

If you are a current print subscriber, you can set up a free website account by clicking here.

Otherwise, click here to view your options for subscribing.

Please log in to continue |

|

If the administration can’t make headway in curbing the cost of pensions and health care costs for retirees through negotiations, then City Council President Steve Merolla said he’s ready to step in and do it by ordinance.

Merolla offered the legislative means of addressing unsustainable retiree expenses following Monday’s council meeting and its anticipated public discussion of a five-year financial projection report.

In an interview Tuesday, Ward 5 Councilman Ed Ladouceur said he hadn’t had the time to review the report prepared by accountants Marcum LLP, but “we all know the elephant in the room.” He named that as pension and healthcare costs for retirees.

Ladouceur said he is contemplating legislation to address those concerns. He called the issue “complicated” and did not define how he would legislatively seek to reduce costs.

As committee meetings extended beyond 10 p.m., Merolla postponed discussion of the Marcum report to the Sept. 4 meeting.

That was a good thing, as many of the audience who had expected the meeting to start at 7 p.m. had left. Additionally, the 36-page PowerPoint presentation had only been sent to council members electronically at 4:15 that afternoon.

Even with such short notice, council members and those in the audience with copies found projections disturbing and, if anything, rosier than what the city faces.

“I don’t think anybody who looks at the numbers doesn’t see red flags,” Merolla said.

The Marcum report said what the city faces can be compared to a household with an annual income of $75,000 and secured debt of $15,000 owing $240,000 on their credit card. The report puts the retired employees’ healthcare budget at $9.27 million this year.

“If we don’t make decisions, someone [a court appointed receiver] will make them for us,” Merolla said.

Specifically, Merolla said the city couldn’t sustain paying retiree health care benefits without a co-pay and with prescription caps.

“You can’t retire and not pay co-pay,” he said. “It’s not sustainable.”

Merolla pointed out that he has been sounding the alarm for years.

“I was Chicken Little and the sky was falling,” he said. He added that the status quo “ostrich policy of the head in the sand can’t continue.”

Former councilman and School Committee Chairman Robert Cushman, who was prepared Monday night to present his own forecast of city finances, found the Marcum report lacking in its assumptions. He said it appears the report failed to consider that firefighters have been without a contract for nearly two years and once an agreement is reached projections won’t be accurate. He also feels the projection doesn’t account for the costs of addressing the city’s aging infrastructure – roads, sewers and water – nor the need to update technology.

“To say nothing is going to change is totally unrealistic,” he said.

Cushman called the Marcum report a “snapshot in time” that makes the problem appear less than what it is.

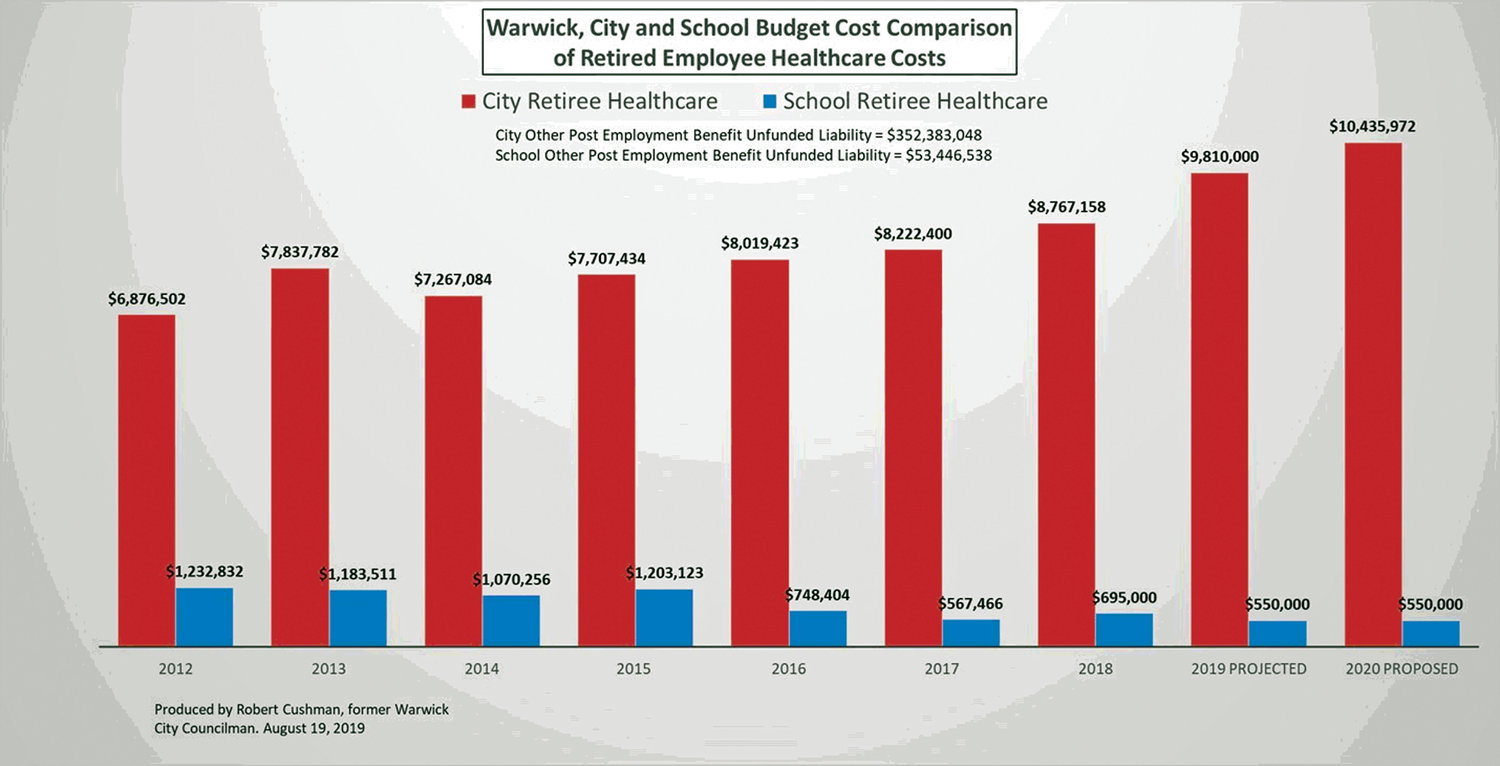

Cushman’s report, summarized in five pages of graphs, depicts retiree employee expenses – which were 19 percent of the budget in 2004 – as now being 29 percent of the budget. On the Fire Department alone, active employees are costing the city $18.6 million while pension expenses are an additional $19.4 million.

One of the most striking graphs is the comparison of city and school retiree healthcare costs. The 2018 city costs were $8.7 million compared to school costs of $695,000. Cushman’s projection for 2020 takes it to $10.4 million for the city versus $550,000 for schools.

Asked about legislative action to enact changes in pension benefits – as was done in 2011 when the council approved the Tier II pension system for municipal employees hired on July 1, 2012, and thereafter – Mayor Joseph Solomon said Tuesday that contract negotiations continue and that under legislation he spearheaded, any agreement reached by the parties will be presented to the council for its action.

“I’m not looking for grandstanding, I’m looking for results,” he said when asked if legislation, rather than negotiations, could be used.

“I’d be very surprised if the mayor is not aboard with ordinances if he can’t negotiate,” Merolla said.

Solomon downplayed what some council members are portraying as a rift between the former council allies. Solomon said he would take Merolla’s calls whenever they are made.

“I don’t get personal,” Solomon said.

Nonetheless, it was clear from Monday’s meeting that Merolla is not being kept abreast of administrative thinking on bonding repaving programs.

Solomon said he read through the Marcum presentation.

“We’re all aware of what areas have to be addressed,” he said. Later he added, “It’s not the Bible you can follow.”

16 comments on this item Please log in to comment by clicking here

Warwick_Resident1998

What cracker-jack box did Merolla get his law degree from?

He really thinks he can write an ordinance which will override a contract?

Make your changes the right way, that way you don’t cost the city extra money, like the decision to appeal tier II with the FD.

Thursday, August 22, 2019 Report this

Daydreambeliever

As I've said before when Merol!a and Ladocuer followed by Travis, Solomon, Pisitauro, Colantuono, Donovan, Gallucci and I'm sure others give up there FREE Lifetime Health Insurance for part time work then come to the unions.

Lead by example instead of always passing the buck.....hypocrite !!!!!!

Friday, August 23, 2019 Report this

Reality

Thank you Councilman Merolla for addressing this issue. For years concerned taxpayers brought these outrageous over the top pension and healthcare benefits to Avedisian's attention and Scottie turned deaf ears. Scottie's answer to the problem was to enhanced them.

Lifetime healthcare has to be eliminated. Caps have to be placed on pensions. No pension should exceed the max. social security benefit of $2861 per mo or $34,300 per year. Retirement benefits should be calculated on one's entire working career like social security and not the last few years of employment that increase benefits.

Prescription drug benefit should be stopped immediately. Healthcare co-pays for active employees should be set at 30% for a start. Retired employees should pay 50% on healthcare benefits with a gradual scale to eliminate them entirely in 7 yrs.

It's time city employees start living in the real world.

Friday, August 23, 2019 Report this

Apple_martinis

NO eliminations of existing programs, NO significant changes, or additions of new programs are contemplated according to the report but it does promise a 4% tax increase each year indefinitely.

Merolla is right on one thing, if they don't make decisions, someone else will make it for them.

I've come to the conclusion that the citizens in this state are lazy, brainwashed sheep who have a high tolerance for tax theft... because who in their right minds keeps voting in the same people (for decades) who continue to increase your property taxes for absolutely nothing in return? This goes for RI as a whole. I say vote all of these malignant tumors out of office.

Friday, August 23, 2019 Report this

Cat2222

It is astonishing that all of them stood by silently when they knew decades of contracts would lead us to this place. I am rather disgusted and cannot view any of them as trustworthy at this point.

Friday, August 23, 2019 Report this

Apple_martinis

What some readers might not realize is unfunded liabilities are a huge problem all across the United States. California, for example, has the highest unfunded liability hovering close to a TRILLION dollars. WA, CT, MA, TX I believe top off the top 5 worst unfunded pensions systems in the US.

Arlene Violet wrote a good article on our unfunded pension liabilities here: http://www.valleybreeze.com/2019-05-08/north-providence/arlene-violet-pension-liabilities-will-swamp-rhode-island#.XWBIbEJ7mtg

The biggest problem I have with our city council is that good citizens have been screaming, literally screaming, consistently for almost 10 years about this financial crisis. Those long standing council members (and a recently elected mayor) have known about this problem for a decade or longer and and have - done - nothing.

Friday, August 23, 2019 Report this

Apple_martinis

Thursday, April 6, 2017 in the Warwick Beacon

It isn’t a pretty picture. According to an actuarial study of retiree health care benefits, the city faces an unfunded liability of $290.7 million this year.

That figure contained in reports prepared by Jefferson Solutions had a chilling effect on the City Council Monday night. Ray Cerrone of Jefferson went through the report that is required under Government Accounting Standard Board Statement No. 45, commonly referred to as GASB 45. GASB requires municipalities to disclose obligations for post-employment benefits (OPEB), which other than pension payments are health care benefits in the case of Warwick.

Unlike pension payments that the city saves for by paying more into pension accounts than it takes out, no such fund exists for retiree health care costs that continue mounting with higher health care expenses (about $9,500 for an individual plan and $23,000 for a family plan for retirees under age 65) and the growing ranks of retirees.

Mayor Scott Avedisian considering budgeting funds to start such a trust, but the amounts were small and the council never went ahead with a plan.

In an email response to questions as to how to deal with the unfunded liability, Avedisian said Wednesday, “As you know, I have been trying to several years to create an OPEB trust at the Rhode Island Interlocal Risk Management Trust. The Trust was approved by the General Assembly and the Governor to serve as a fiduciary agent for cities and towns in this matter. What I sought to do was to create a line item in each budget to begin funding OPEB, along with the notion that in 20 or so years, the unfunded liability for pensions will be paid off and we could use that annual appropriation to fund OPEB.”

Avedisian went on to explain, “the idea was to start a trust now and fund it annually until the unfunded pension liability is gone and we could transfer the money into OPEB. In discussion with members of the council and Council President Solomon it was obvious that there was little support for this legislation so I withdrew my proposal.”

As it works now, the city pays the bills amounting to about $8 million for retirees, never putting aside additional funds to build a trust to help pay for the future cost of these benefits. To fund the annual required contribution over a 30-year period, Cerrone calculates the city would need to spend $22 million in the coming fiscal year and adhere to a program of additional expenditures going forward.

Ward 9 Councilman Steve Merolla put the situation in perspective. He said even if the city raised taxes by the maximum 4 percent allowed by state law, it couldn’t fund the OPEB.

“We’ll never be able to pay this off,” Merolla said.

Cerrone didn’t argue, although he offered some options going forward, which he said would probably end up in court. They included an age cutoff at 65 years old when people become eligible for Medicare. Teachers who are in a state plan face such a cutoff. Some plans also provide for the retiree to stay in the municipal health plan at their own cost or providing an annual maximum health care payment. Other plans offer terms on health care, limiting coverage to just the retiree and not his or her family and carry co-payment requirements.

About two years ago, Cerrone provided the council with a more detailed list of 11 actions the city could take to reduce the cost of retiree health care benefits.

On Wednesday Finance Committee Chair Ed Ladouceur questioned why the administration hasn’t followed up on those recommendations. At the very minimum he thought the city should be placing restrictions on retiree health care benefits for new hires.

“Lifetime health plan makes no sense. Health care benefits should be capped and it should only be for the retiree only [no family plan],” he said.

“We can throw millions and millions at the school department or some of other things and that’s not going to fix it. Long-term sustainability has got to be dealt with right now,” he said.

Of the unfunded OPEB liability, the lion’s share – 70 percent – is made up of uniformed retirees. As Cerrone pointed out, depending on their contracts fire and police are eligible for retirement after 20 or 25 years of service. This means a municipality that has given lifetime health coverage, is paying for that benefit starting in many cases at an age in the mid-40s until death. Even when a retiree dies, the cost may not cease since by contract the benefit is passed on to the surviving spouse.

Cerrone calculated the health care cost of a typical retired Warwick firefighter at $568,000. That number left the council aghast.

“It becomes a really significant obligation,” said Cerrone.

Ward 1 Councilman Richard Corley wanted to be certain he understood the magnitude of the problem. He questioned whether this has nothing to do with pension payments and that nothing is being put aside to pay for the future cost of these benefits.

“That’s right,” said Cerrone.

And then providing the only moment of levity, Corley responded, “Oh, sh--.”

************

So back in 2015, Cerrone provided the council with a more detailed list of 11 actions the city could take to reduce the cost of retiree health care benefits and what changes since then have been implemented? ---> insert sound of crickets here <---

Friday, August 23, 2019 Report this

Bob_Cushman

City council needs to file legislation declaring a fiscal emergency in the city. This would give the city the legal president to make unilateral cuts to these benefits, including suspending pension Cost of Living Increases and imposing cost sharing on retiree healthcare. S 50% co-pay would result in $5 million annual savings.

If the city mirrored school retiree healthcare benefits almost $10 million could be saved each year. Over 5 years that would be $50 million that could be reallocated to educational and city programs and services that are needed.

The fact that the council is considering writing ordinances to control these costs is a major development that should be supported by Warwick taxpayers.

Friday, August 23, 2019 Report this

Reality

Councilman Merolla is to be commended for introducing these ordinances.

If Solomon was on the council still, he would be joining Merolla with his initiative. Unfortunately, Mayor Solomon has followed the Avedisian playbook i.e. give the unions everything they want. Solomon has been a big disappointment.

Solomon's tenets have been cast aside for political gain.

Warwick's actuary stated in 2016 that a Warwick fireman will get $568000 in healthcare benefits in retirement. Couple that with pension benefits the taxpayers will pay over $1000000 for a retired fireman.

Maybe the new recruitment poster should be .....Become a Warwick Fireman and become an instant millionaire."

This has to stop now.

Sunday, August 25, 2019 Report this

Cat2222

" In discussion with members of the council and Council President Solomon it was obvious that there was little support for this legislation so I withdrew my proposal.” WHY?

Mayor Solomon, I feel deceived by your campaign. You are a huge part of the problem and you are doing what is best for you and not the people of Warwick.

Monday, August 26, 2019 Report this

Apple_martinis

Cat - I started attending city council meeting last year. Let's face it. Warwick's citizens are about as disengaged as you're going get and our local government knows this. Only until the citizens of Warwick start to show an interest in how our taxpayer dollars are being spent, the malfeasance and literal theft will continue until there are no more ways to increase revenue via taxes and fees and the city is taken over in receivership. When that happens, everyone loses.

Monday, August 26, 2019 Report this

Bob_Cushman

This is the Joe Solomon we need as mayor as the guy I voted for. What happened to this point of view from 2012?

http://www.warwickonline.com/stories/mayor-downplays-solomon-alarm-on-city-finances,71154

Mayor downplays Solomon alarm on city finances

Posted Thursday, May 17, 2012 1:00 pm

John Howell

Ward 4 Councilman Joseph Solomon has joined the drumbeat of former Ward 1 Councilman Robert Cushman that maintains that the city’s financial condition is worse than the administration would have taxpayers believe.

Mayor Scott Avedisian, however, maintains that the city is on sound financial footing.

Citing declining city assets, as defined in the city audit, Solomon introduced a resolution at Monday’s City Council meeting calling for the creation of a blue ribbon fiscal commission to research the issue and turn around the city’s finances. Solomon said he has the names of people in the private and quasi-public sectors who he feels would “think outside of the box” in coming up with creative ideas, but he would like to see who might step forward to volunteer their services.

In a press release disseminated to news outlets across the state Monday night, Solomon said that the city’s net assets fell from $79.2 million to $61.4 million in the fiscal year ending July 1, 2011. Further, he points out that since 2007, city assets, which he calculated by subtracting liabilities, have fallen by $129.6 million.

“I have repeatedly warned the administration, my colleagues on the City Council, the media and taxpayers that Warwick’s financial condition is deteriorating—and deteriorating fast,” Solomon asserted.

In a press release on Tuesday, Avedisian responded that the net assets reflect the city’s net worth and that has no relationship to the fund balance.

“In fact, the fund financial statements provide a more accurate representation of the city’s cash position and current fund balance,” reads the release. The fund balance, or accumulated surplus, was $5.9 million as of July 1, 2011.

He said the decline in assets is primarily due to two accounting accruals, which are required by the Governmental Accounting Standards Board.

In a telephone interview Tuesday, Solomon said, “we’re not Central Falls, but we’re headed in that direction.”

Solomon’s warning has a familiar ring to what Cushman has been saying.

Cushman has focused his attention on city pension funds and recently testified before the Rhode Island Municipal Pension Study Commission.

In a press release issued following that hearing, Cushman says, "We are clearly in a crisis situation in Warwick, with the lion share of our tax dollars going to fund an unsustainable pension system and employee benefits program. Our city is doing what Providence did years ago, ignoring the problem and kicking the problem down the road until it blows up on someone else's watch. Politicians come and go … but those of us who live here in Warwick are going to be stuck with a huge bill if we don't get serious about addressing this crisis now."

That’s not the way Avedisian sees it.

In an eight-page letter dated May 9 to Rosemary Booth Gallogly, chair of the pension study commission and state director of revenue, Avedisian spells out pension reforms initiated by his administration and enacted prior to General Assembly approval of state pension reforms. He also lists funding rations for the city’s four pension plans that are all above 70 percent, with the exception of the Police/Fire I plan that is at 22.3 percent. The mayor notes that the city is in the 18th year of a 40-year funding plan for that system.

Referencing the information provided by Cushman, Avedisian writes, “however, the information presented during the public comment portion of your meeting also includes the addition of Other Post Employee Benefits (OPEB) into this equation – a move that is solely intended to make the city’s numbers look bad.”

The mayor goes on to say the city has heeded the recommendation of pension professionals and that he believes the actions taken “should show you and your fellow commissioners that we have put together a good, effective plan for this city.”

Cushman, who agrees with Solomon’s conclusion, said Tuesday that the city’s declining assets “all ties in together” and is part of a bigger picture where legacy health and pension benefits promised to employees will outstrip the taxpayers’ ability to pay.

“Every year it is getting higher and higher,” he said of OPEB costs.

Cushman said it is his intent to show the true costs facing the city.

“It is not just the pension problem. You have to include it all, include the OPEB,” he said.

Based on his calculations, Cushman says that only about 35 percent of the city’s total liabilities are funded.

The mayor said the city started accruing the OPEB liability in 2008, as amortized over 30 years as determined by the actuaries. He goes on to say that the city’s actuary recommended continuing with the 40-year plan to address Police/Fire I, even though “technically” it is not in compliance with governmental accounting standards requiring an amortization period not exceeding 30 years.

These two components account for approximately $20 million to $23 million per, the mayor says. “Without these requirements,” Avedisian said, “the city’s net assets would actually be increasing.”

In a follow-up call Tuesday afternoon, Solomon questioned the mayor’s characterization that net assets are not a true indicator of the city’s financial health. Quoting page 7 of the document, he reads, “increases or decreases in the city's net assets are an indicator of whether its financial health is improving or deteriorating, respectively.”

“I don’t want to cross horns with the mayor,” Solomon said. “I want to be a part of a solution to this problem. I want to correct it.”

Monday, August 26, 2019 Report this

Bob_Cushman

Cat: just want you to be aware that the legislature that was proposed by former Mayor Avedisian regarding unfunded healthcare liabilities (OPEB) was a fraud. It’s was a Ponzi scheme.

That’s why Solomon and the rest of the council rightfully rejected it.

Please review my testimony on the legislation at this link:

https://youtu.be/HYx3zVLbdOU

Monday, August 26, 2019 Report this

Bob_Cushman

Louise401: I have a copy of the 11 actions city could take.

Some are good, others bad.

Here they are:

JEFFERSON SOLUTIONS, INC.

14 Brittany Oaks Clifton Park, New York 10265 518-461-7805 www.gasb45.com

May 26, 2015

Mr. Ernest Zmyslinski, Director of Finance City of Warwick Rhode Island ernest.m.zmyslinski@warwickri.com 3275 Post Road

Warwick, Rhode Island 02886

RE: Funding OPEB Liability Dear Ernie:

I wanted to respond to your email dated May 19, 2015 regarding the use of an OPEB Trust and partial funding of the City’s OPEB liability.

In summary, your email contained the following questions:

1. What position does Jefferson Solutions, Inc. take with respect to OPEB Trusts?

2. What position does Jefferson Solutions, Inc. take with respect the city contributing $200,000

to a state-wide OPEB trust?

These are excellent questions to be asking with respect to careful management of the City’s OPEB liability. Our response follows:

POSITION ON AN OPEB TRUST: Jefferson Solutions, Inc. would support the City’s decision to make contributions into an OPEB trust if it is able to afford the cost. Pre-funding the OPEB liability can have a significant impact on the overall liability and costs associated with OPEB due to the fact that it may allow an entity to increase its assumed discount rate with respect to the funds that have been set aside in the trust.

Pre-funding OPEB could allow the City to adjust the discount rate to the level of the expected return on the assets placed into the trust. Typically, a well-managed OPEB trust would earn rates of return similar to those earned on the State Employee Pension Fund. Presently, the City uses a discount rate of 4.00% in determining its OPEB liability and Costs. The State Employee Pension fund used a 7.50% assumed rate of return in its actuarial report dated June 30, 2015.

Since there is an inverse relationship between the assumed rate of return and the OPEB liability and costs, pre-funding and taking advantage of higher assumed rates of return could have a significant impact on the City’s OPEB provided that the contributions are material.

POSITION ON MAKING A $200,000 CONTRIBUTION: Jefferson Solutions, Inc. does not want to discourage the City from making contributions to an OPEB trust in any amount.

However, it making a decision on the funding level for the City, it is important to focus on the results in the June 30, 2014 report to evaluate if the amount funded would make a material difference.

A brief recap from June 30, 2014 report is as follows:

The Annual OPEB Costs .............................................................. $23,100,000 The amount Paid for Retiree Benefits ............................................. 7,300,000 Leaving:

An Unfunded OPEB Cost of .................................................. $15,800,000

This unfunded portion of the OPEB costs is attributable to the active employees.

Proposed Funding ........................................................................... $200,000

Increase in OPEB Funding ....................................................................... 1.2%

If the City placed $200,000 into an OPEB Trust this would equate to funding 1.2% of the unfunded portion of the OPEB costs. In our opinion, this would be relatively immaterial, but it is also a step in the right direction. We also believe that this level of funding would not provide an increase in the discount rate due to the limited amount.

Jefferson Solutions, Inc. has prepared an attachment to this letter with suggestions on how to manage the OPEB liability. We would suggest that the City consider some of the alternative strategies mentioned in the attached.

I am looking forward to meeting with the City Council at the June 8, 2015 meeting. I will be happy to address their concerns with respect to the most recent report. I also encourage discussion on the attached strategy.

Very truly yours,

Raymond R. Cerrone, CPA, EMT-1 Principal

Jefferson Solutions, Inc.

Suggestions for Managing the Liability

Mitigating strategies for Reducing the Impact of OPEB:

We encourage the City of Warwick to consider the following suggestions for reducing the OPEB liability and related costs. These suggestions should be taken into consideration with the assistance of the City’s legal counsel and in cooperation with the various bargaining units.

1. Make Greater use of Medicare:

According to the GFOA, jurisdictions like the City of Warwick can leverage Medicare to lower OPEB costs:

Many municipal governments can use Medicare to lower their OPEB costs, according to Moody’s Investors Service. For retirees over age 65, this liability consists primarily of Medicare premium subsidies and supplemental health insurance benefits.” Leveraging Medicare for these employees is worth considering because “even small reductions in the cost of health benefits for Medicare-eligible retirees can have a considerable impact on future costs because savings compound over retirees’ increasingly long lifetimes.”

2. Consider funding the Annual Required Contribution:

One of the most important factors in determining OPEB liabilities and costs is the interest rate used to discount future benefit payments to the present. As a general guideline, a 1% decrease in the discount rate may cause a 15% - 20% increase in liability and the ARC. GASB rules state that the discount rate to value OPEB liabilities must reflect expected returns on assets used to pay benefits. If OPEB liabilities are not funded in advance, this means the discount rate would be the expected return on the assets of the sponsoring employer. Statutory restrictions on fund investments (and the fact that few entities have extra funds that can be invested) likely means a low rate of return on assets. This results in the mandated use of a low discount rate for OPEB liabilities (and correspondingly high liabilities and costs). On the other hand, if the OPEB liabilities are funded in advance in a separate trust dedicated to provide OPEB benefits, the assets may be invested in longer- term investments with higher expected returns.

The City of Warwick should consider funding of the annual required contribution in an amount that is greater then what is required under the current pay-as-you-go practice. Funding a larger portion of the ARC will results in increasing demands on the budget while accomplishing two other important goals:

(a) Increasing the discount rate and lowering the cost for OPEB in the long run; and

(b) Providing future retirees with some level of assurance that the resources to pay the benefits will be available at a future date.

3. Change the plan for new hires:

The easiest long-term reform for retirement benefits is to reduce them for new employees. Unfortunately that won’t save much money for years to come, but it’s a start. With private-sector employers rapidly abandoning retiree medical benefits, there is little competitive pressure to maintain traditional OPEB plans. A modest defined contribution plan for retirement health savings is usually all the market requires. Some employers are providing employee-only coverage for new hires.

4. Cap the benefits:

With medical costs outstripping general inflation by two or three times each year, the biggest move employers can make is to put a dollar ceiling on the benefit and index it to the CPI. This single action has huge actuarial cost-reducing benefits.

5. Require employee contributions:

Most public employees, especially the older ones, know the value of their OPEB benefits. It’s only fair that they pay part of the costs. If you are freezing salaries, you can’t ask for much, but a symbolic sliver of cost-sharing can be expanded later when the economy gets better.

Presently, the City covers 100% of the cost for both the retired employee and any covered dependent.

Continued

Suggestions for Managing the Liability (Continued)

6. Fund the plan actuarially:

Most public employers with massive OPEB liabilities have not even set up a trust fund to pre-fund the benefits. This ostrich-like behavior guarantees that the problem will worsen. Even if budgets are tight, it makes sense to make partial payments toward the actuarially required contributions and then “ramp up” a little each year. Employees can’t be asked to contribute if there’s no trust fund in place.

7. Install a “narrow network” HMO:

Along with higher deductibles and co-pays, many employers have also installed a narrow-network HMO as the primary health-care benefit for their employees. Narrow networks exclude high-cost medical providers and thus cut premium costs. This can then become the basis for the retirees’ OPEB benefit as well, which can cut costs by 25 percent in some locations.

8. Sell bonds to fund one-third of OPEB liabilities:

Nobody can tell for sure whether the stock market’s latest swoon was a bottom, but interest rates are now near their lowest levels in a century. That enables some public employers to sell taxable municipal bonds for as much as a third of the total OPEB plan liability, and invest the money in the stock market at depressed levels. For more on this strategy and pitfalls to avoid, see my article, Benefits Bonds Revisited, in the Public Money section on Governing.com.

9. Buy out the benefits:

Beverly Hills, Calif., won national attention and a professional association award for its innovative solution to skyrocketing OPEB costs. The big idea: Get out of the business of guaranteeing retiree medical benefits the city can’t afford. First, the city set up a defined-contribution OPEB plan for new employees. Then it sold a bond issue at 4.5 percent and used the money to fund a voluntary exchange program in which current employees could cash out the actuarial value of their previously earned OPEB benefits and receive an employee health savings account plus a package of cash and deferred compensation. More than half of the eligible employees made this election, which will save the city millions of dollars. It’s been so popular that employees who didn’t take the original deal now want in.

10. Reform Benefits for Incumbent Employees:

Legal issues are likely to arise here, as each state has its own laws (with limited case law) regarding the vested rights of employees to receive retiree medical benefits. In some states, the OPEB benefit is a gratuity and can be cancelled or modified by the plan sponsor. In others, however, the courts might find that employees have vested rights similar to those regarding pension benefits.

Beyond legal concerns, there are also moral and morale issues to consider when modifying benefits of incumbent employees. For example, a fully vested employee who has satisfied all the age and service requirements for a full OPEB benefit has a strong claim that the benefit cannot be reduced.

At most, public employers in such cases might attempt to raise the distribution age by a few years, increase the employee contribution, and cap the annual benefit with a CPI escalation limit. Such measures can mitigate costs while still recognizing the employees’ legitimate claims to the core benefits they have already earned through prior service.

For younger workers, the employer has a stronger case and an easier path to modifying the benefit structure, if state law allows. In addition to raising the age and service eligibility requirements and establishing a cap (based on a dollar amount or CPI/ inflation) on the annual benefit, OPEB plan reformers can explore the feasibility of restructuring the benefit to a tax-free monthly retirement medical stipend of $10 to $20 monthly for each year of service. Vesting for such employees should be revised upward, in many cases, to strengthen employee retention.

Continued

Suggestions for Managing the Liability (Continued)

11. Consider Labor Relations:

Experienced financial managers know that benefits plan changes can be disruptive in the workforce and cannot be imposed in a vacuum without major repercussions. In states that have strong collective bargaining laws and traditions, these changes must be negotiated.

Even in right to work states that have greater employer discretion, the morale impact of changing benefits must be taken into account. Employees and their labor representatives must first be informed of the long-term true-cost trajectory of their current benefits plans.

If the cumulative costs are unsustainable, employees should be made aware of this unavoidable fact of life and the consequences of inaction. The actuarial data and graphics discussed above should make that picture clear and undeniable.

When confronted with the prospect of a “lost decade” with virtually no salary increases and chronic workforce attrition, many public employees will eventually accept the need for change, especially if the reforms are phased in incrementally and designed thoughtfully. A cohesive labor relations strategy should be developed and must be supported by elected officials to be effective.

CONCLUSIONS:

Many governmental employers have avoided material unfunded OPEB liabilities, but most of those that provide especially generous early-retirement medical benefits and now face a dismal future unless they act soon to mitigate costs. Long-term solutions that affect future employees are helpful, but they typically fail to offset imminent cost increases. Increased employee contributions for OPEB benefits will become far more common in the near future.

Where permitted by state law, public employers are likely to begin restructuring benefits obligations to current employees as well as new hires, and the sooner this process begins, the greater the cost savings. Innovative financial strategies can be considered, but they are, ironically, best suited for those whose balance sheets and operating budgets need help the least, and infeasible for employers that need the most help.

Many public officials will eventually conclude that medical benefits for public employees who retire before attaining Medicare age can be sustained only through employee matching contributions to a defined contribution plan or a very modest defined stipend based on a full lifetime career of public service.

Monday, August 26, 2019 Report this

Apple_martinis

Bob, I listened to the entire video and thank you for your service to the citizens of Warwick. Sadly, all your hopes and wishes have not come to fruition. Not surprisingly, they're are still there and Solomon is now our mayor!

At the end of the video, you talk about education. Did you mean educating the present working employees, the retirees or both? What entity represents the retirees? Has anyone representing the unions (and presumably the retirees) spoken out about this? Or are the current union contracts so iron clad that (their contracts) will literally be impossible to ratify which would explain their silence. I wonder how many retirees have moved out of Rhode Island and truly have not been paying attention to the financial crisis Warwick is facing. Let's all face it, *free* lifetime healthcare is exactly like winning the lottery and nobody on the other side wants to rock the boat.

Monday, August 26, 2019 Report this

Tomhob13

Stop being hypocrites.stop paying lip service.fix the problems or step aside.as they say lead follow or get out of the way.

Saturday, August 31, 2019 Report this