Now that the federal flood insurance program has been extended, Sen. Jack Reed believes that premiums will decline and floodplain maps will more accurately reflect conditions.

Reed worked to pass …

This item is available in full to subscribers.

We have recently launched a new and improved website. To continue reading, you will need to either log into your subscriber account, or purchase a new subscription.

If you are a current print subscriber, you can set up a free website account by clicking here.

Otherwise, click here to view your options for subscribing.

Please log in to continue |

|

Now that the federal flood insurance program has been extended, Sen. Jack Reed believes that premiums will decline and floodplain maps will more accurately reflect conditions.

Reed worked to pass a reformed version of the federal flood insurance program through the Senate on June 29, extending it for five more years. The measure awaits the signature of the president.

The reformed program will improve floodplain mapping, allowing more residents to obtain or renew policies at more affordable rates, says Reed.

Managed by the Federal Emergency Management Agency’s Mitigation Division (FEMA), the National Flood Insurance Program (NFIP) insures property, mitigates flood risk and conducts flood hazard mapping. Government funds insure flood-prone properties in cases where private firms are unable or unwilling to do so, and serve as an alternative to disaster assistance.

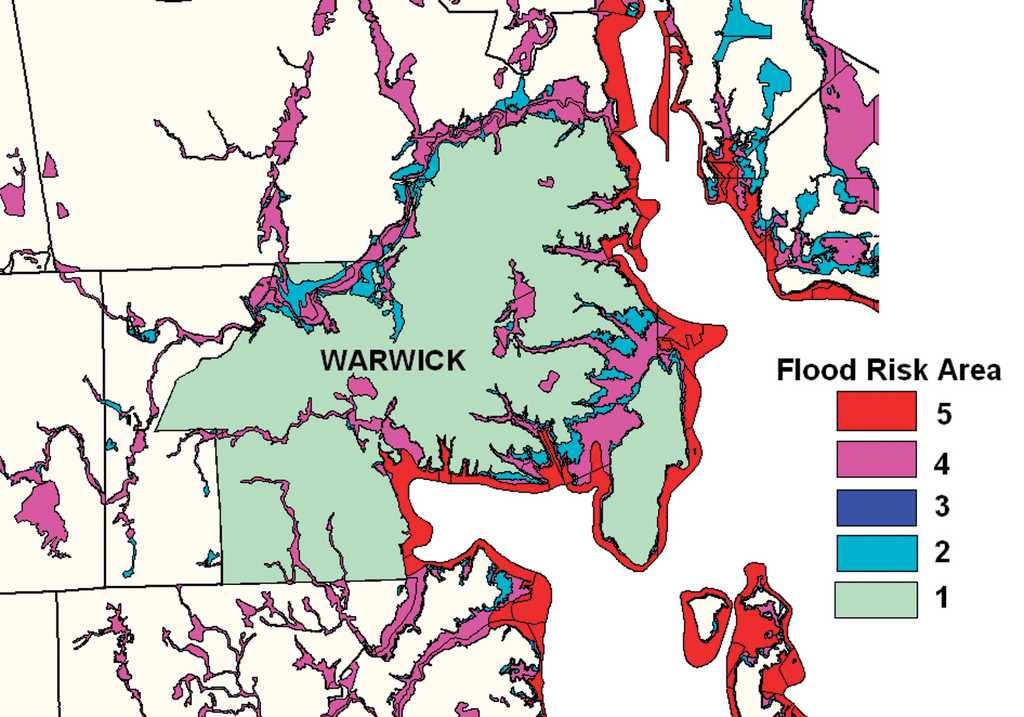

Warwick residents hold 1,903 flood insurance policies, outnumbering all other cities and towns in the state – and approximately 500 of these policies are for properties in areas with no assessed flood risk, says Michelle F. Burnett, floodplain coordinator for the Rhode Island Emergency Management Agency (RIEMA).

A total of $427 million in Warwick properties, structures and building contents are covered by federal flood insurance. This accounts for little over 5 percent of all the city’s property. The value of all taxable property in Warwick comes to roughly $8 billion, according to Tax Collector Kenneth Mallette.

Policyholders in Warwick paid a yearly average of $1,328 in flood insurance premiums, says Burnett. Since 1978, the flood insurance program has processed more than 800 claims in Warwick, paying out more than $10 million.

Warwick Mayor Scott Avedisian supports Reed in the extension of the program.

“We have experienced numerous flood events in the past and know all too well the devastating effect they can have on the economy,” he said in an email.

Avedisian also stands behind the need for up-to-date federal flood classifications.

“We need to make sure that every home is treated fairly and equitably,” he said. “Many residents are paying very high costs due to federal classification.”

Failure to renew the NFIP would have left home closing transactions in flood-prone areas dead in the water – in June 2010, more than 40,000 home sales were stalled due to month-long lapses in the program, according to the National Association of Realtors.

According to Reed’s office, a home with a 30-year mortgage in a 100-year floodplain holds a significantly high degree of flood damage risk in its lifetime – up to 25 percent. That same home in a 500-year floodplain can have a risk of up to 4 percent.

Following record rainfall that caused the Pawtuxet River to overflow in March 2010, floodwaters measuring over 11 feet inundated sections of the city – more than double the regular nine-foot flood stage. To help cover the extensive loss of property and homes, the federal government provided nearly $79 million in grants and loans.

Warwick’s 2011 Hazards Mitigation Strategy, which outlines natural disaster risk and loss prevention for municipal uses, showed that flooding events over the last 60 years in Kent County have caused more damage than all others combined, including blizzards and windstorms.

The program, authorized under FEMA, insures more than 16,000 property owners in Rhode Island, covering up to $3.9 billion in structures and personal property across the state.

Federal law also requires FEMA to compile flood insurance rate maps, or FIRMs, which utilize geological data to set premiums.

Updated Digital Flood Insurance Maps (DFIRMs) of the city’s coast, set to roll out by spring of 2013, will include new topographical models, using measurements made by advanced fly-over light detection and ranging instruments (LIDAR).

FEMA separates 100-year floodplains into special flood hazard zones based on their particular source of deluge, whether from coastal storm surge and waves (VE zones and AE zones), or inland pond or river flooding (A zones).

In the United States, the NFIP mandates flood insurance for any property owner with a home in a special flood hazard zone, but only if their mortgage came from a federally regulated lender. Otherwise, homeowners, even those in low risk zones, may purchase flood insurance at their leisure.

All 39 cities and towns in the state are enrolled under the NFIP, meaning any Rhode Islander can qualify.

According to the NFIP, a flood insurance policy can cover up to $250,000 in individual structural flood damage, and up to $100,000 in personal possessions. Damage sustained in a declared disaster event, like the March 2010 floods, may be covered by FEMA – but payouts only compensate up to $30,000. The uninsured, flooded out in an undeclared disaster, shoulder the costs of destruction alone. According to a FEMA flood insurance fact sheet, most homeowners’ insurance policies do not cover flood insurance.

Timely reauthorization of the program is essential for flood-threatened Americans who have yet to enroll.

“During times of short-term lapses, you can’t buy flood insurance. If you’re looking to renew or start a policy, you’re stuck until the program starts again,” said a contact at Sen. Reed’s office.

With FEMA already in the process of modernizing antiquated FIRMs, Reed’s reformed NFIP will do more than extend coverage – it would help Americans be more aware of their actual flood risk, with FIRMs reflecting more realistic insurance rates.

“[The] legislation … would modernize maps used to designate flood zones as well as determine rates and set premiums more in line with actual risks,” read Reed’s press release, “and to improve the maps the federal government uses to predict the risk of flooding.”

Reed’s office contact reiterated that the reforms help to protect the Americans’ ‘right to know,’ saying, “Risk isn’t shown as well as it should be [in current FIRMs]. If you live on or close to a flood plain, that’s information you should be able to access. There are also people who are at risk and do not know it.”

By making accurate maps, it is not only beneficial to private insurers and homeowners, but to community leaders as well –officials who are very deeply involved in city planning. “That way, plans on appropriate zoning and emergency response can be made,” he said.

Homeowners are encouraged by both the RIEMA and FEMA to purchase flood insurance. FEMA’s flood insurance fact sheet is an important tool for prospective policyholders, and can be found through warwickri.gov (search keyword: flood insurance). Policies may be purchased through agents working in more than 20,300 communities around the country. To contact your local insurance provider, visit FloodSmart.gov or call 1-800-427-2419.

Comments

No comments on this item Please log in to comment by clicking here