In 2006, Peter Appollonio and his wife found the house of their dreams on Foster Street in Conimicut.

The asking price was beyond their range – $580,000 – but they thought there was no harm …

This item is available in full to subscribers.

We have recently launched a new and improved website. To continue reading, you will need to either log into your subscriber account, or purchase a new subscription.

If you are a current print subscriber, you can set up a free website account by clicking here.

Otherwise, click here to view your options for subscribing.

Please log in to continue |

|

In 2006, Peter Appollonio and his wife found the house of their dreams on Foster Street in Conimicut.

The asking price was beyond their range – $580,000 – but they thought there was no harm in looking. They loved it. And when they told the realtor all they could afford was $400,000, they were laughed at. It looked like the house would remain a dream.

However, the Appollonios had bank approval for a $400,000 mortgage and while there may have been many lookers, the realtors realized they had a potential buyer.

They got the house for $430,000.

The house has been everything they had hoped for. It was built to survive hurricanes and northeasters that have flooded Conimicut in the past and caused evacuation of the low-lying peninsula. The living area and utilities are all well above the base flood elevation (BFE) level. The hot water heater is 18 feet above the BFE. The washer/dryer is even higher and the heating and air conditioning is on the roof, three stories above ground.

This is a house that was built to meet Federal Emergency Management Agency (FEMA) recommendations.

Appollonio calls Conimicut “the hidden gem.” He loves the sunsets and the views of the bay and the salt marsh not far from his property. He says the point is like “one big family.” People are friendly. His parents live a couple of blocks away on Point Avenue.

“I’m really happy down here,” he said Saturday morning. Appollonio had just completed his shift as a West Warwick police officer and was closing his gate. The family dog, Sam, greeted him.

But the dream house has become a flood insurance sinkhole.

Now Appollonio doesn’t see a way out, regardless of how many special details he works to bring in added revenue.

“They’re killing me,” Appollonio says of insurance premiums that started at $4,100 and have escalated to $9,400. Between that and the taxes, Appollonio has put off any thought of special projects.

“I have worked hard for what we have and I will have to work harder to hold on to it,” he said.

Appollonio is one of 1,887 Warwick homeowners with flood insurance – the larger part of the 2,454 Kent County residents with policies. Of the county totals, 1,254 policies are subsidized, meaning those rates have been artificially low, based on the exposure to risk faced by those properties.

A casual survey of more than seven other Conimicut property owners Saturday found premiums ranging from $400 to $3,500. Many of the properties were on the beach and had not been designed to withstand the flooding and wave action of a severe storm. Many of these property owners have been “grandfathered” into their premiums.

That situation is going to end under the Biggert-Waters Flood Insurance Reform Act of 2012, which reauthorized the National Flood Insurance Program (NFIP) through Sept. 30, 2017.

This Wednesday, from 4 to 9 p.m. in City Council Chambers, FEMA and the Rhode Island Emergency Management Agency (RIEMA) will conduct an informational meeting on the new law.

It’s going to bring some big changes that some city officials fear will force long-time residents out of their homes. It could also mean relief for homeowners like Appollonio.

According to a press release issued Friday by RIEMA, “The NFIP reauthorization included a number of reforms aimed at making the program more financially and structurally sound, some of which have already started to affect NFIP policy holders in the state. The intent behind the new legislation was to eliminate artificially low rates and discounts for some policyholders that are no longer sustainable. The new law aims to reflect full risk and phase out subsidized rates for certain types of policies, including non-primary/secondary homes and businesses and properties that have sustained severe or repeated flooding.

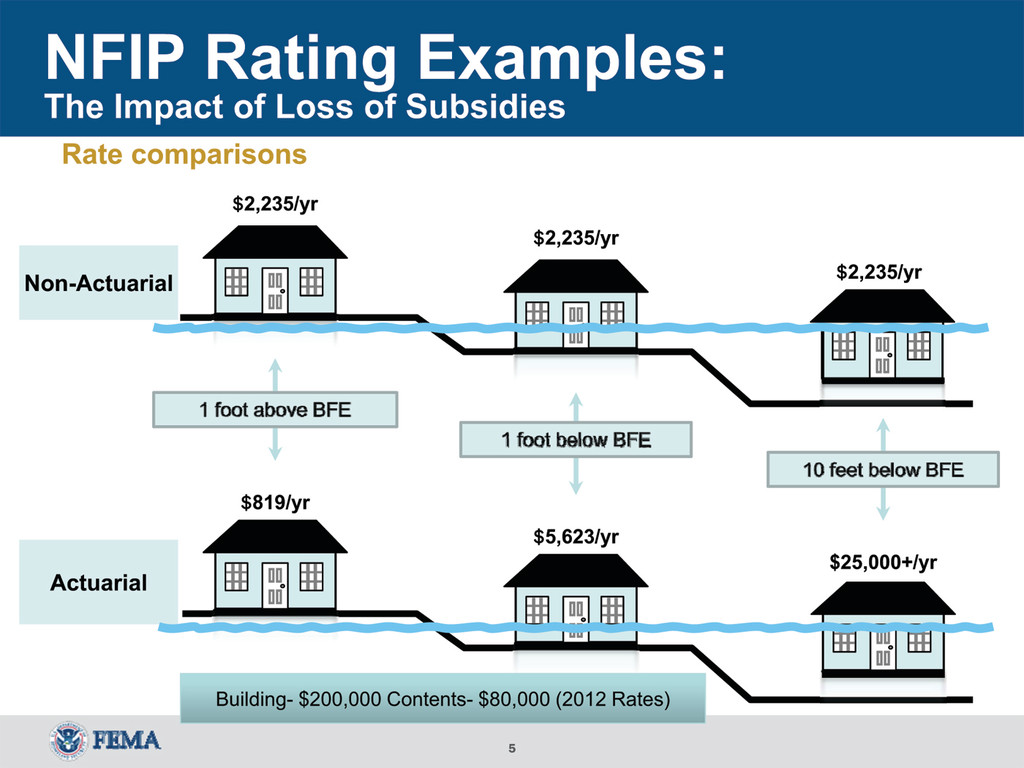

According to an illustration released by FEMA, the loss of subsides could reduce the premium for $200,000 of building insurance and $80,000 on contents on a property one foot above the base flood elevation from $2,235 to $819. By the same token, the owner of a property at 10 feet below the flood elevation would see the premium climb from $2,235 to $25,000.

According to RIEMA, the phase out of subsidies would occur over a five-year period, at 20 percent a year, starting in 2014. RIEMA doesn’t say how the law would impact non-subsidized rates and whether they could expect a decline in premiums and within what period of time.

City Planner William DePasquale is concerned for those homeowners who won’t have the means to either alter their houses to make them less prone to flooding and storm damage or to pay the new premium. As most lending institutions demand flood insurance to secure loans in flood zones, he imagines situations where people will be forced to sell and, yet, because of the high cost of insurance, be unable to find buyers.

In addition to the law, DePasquale notes new maps designating flood elevations are altering the areas affected. In some cases, areas once within a flood zone are no longer in it. New areas have been added and, in some instances, designations have been changed from AE Flood to VE Flood. The VE designation, which covers most of Conimicut and low-lying area of Oakland Beach, takes into account wave action.

“There are changes throughout the city,” DePasquale said.

In a release issued Friday, Mayor Scott Avedisian urged people living in flood zones to attend tomorrow’s meeting. Citing the short public notice, he said he has also requested a second meeting for Kent and Providence County residents.

Appollonio, who is carrying a $260,000 mortgage on his home, looks forward to the day when he has paid off the mortgage. If premiums are what they are today, he would then drop the policy and self-insure. In fact, if he could do that, he would do it now.

“With what I pay in premiums, I could build my house twice over [in the wake of the storm],” he said.

Another Conimicut property owner, Ralph Bozzi, said the high cost of flood insurance has dampened efforts to renovate properties while stopping projects, including new construction, that would meet flood codes.

Comments

No comments on this item Please log in to comment by clicking here